The Amazon marketplace is consolidating. Not slowly, not gradually — it’s happening now, and the data from 2025 makes the shape of it unmistakable.

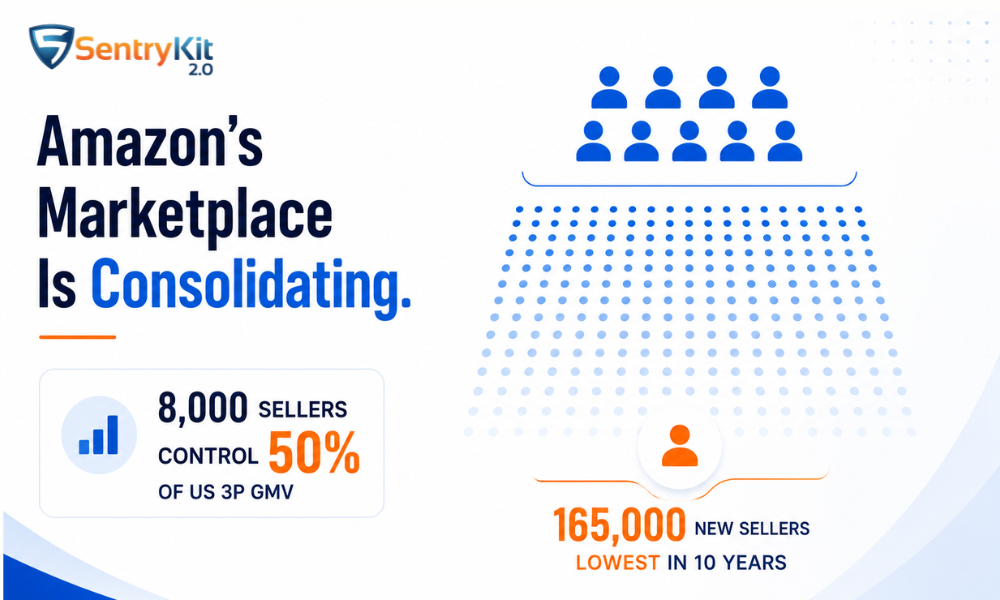

165,000 new sellers launched their first Amazon.com listing in 2025. That’s the lowest figure in a decade. Down 44% year over year. Down 73% from the 2021 peak.

At the same time: 100,000+ sellers are doing $1M+ per year. 235 sellers crossed $100M. Fewer than 8,000 sellers drive half of all US third-party GMV.

The way I read this data, it describes a two-tier marketplace in the process of hardening. The numbers aren’t a snapshot of a healthy middle. They’re evidence of a structural shift in who competes, at what scale, and with what tools. Every seller needs to understand which tier they’re building toward — because the answer changes how you should operate.

The Number Most Sellers Get Wrong

Almost every piece of content on this topic gets the baseline wrong in ways that matter. So before anything else, here’s the correction.

You’ll see “9.7 million Amazon sellers worldwide” cited constantly. That figure includes every seller who has ever registered an account, including dormant accounts, abandoned experiments, and sellers who listed a single product in 2019 and never logged back in.

The operative number is active sellers. By a feedback-based definition — sellers who have received at least one piece of buyer feedback in a recent trailing period — the global active seller count sits at approximately 1.65 million at the end of 2025. That’s down from 2.4 million in 2021.

For the US specifically, the picture is even sharper. If you apply a strict definition of active — sellers with a meaningful, current selling presence on Amazon.com — you’re looking at roughly 500,000. Not 1.1 million. Not 2 million.

Why does this distinction matter? Because when you hear “millions of sellers,” your mental model of the competitive landscape is wrong. You’re not competing against 9 million businesses. You’re competing against a smaller, more concentrated, better-capitalized pool. That changes the analysis.

New Registrations Hit a Decade Low — and What That Actually Means

Here’s where it gets interesting.

165,000 new sellers launched their first listing on Amazon.com in 2025, according to Marketplace Pulse. That’s a decade low. Down 44% from 2024. Down 73% from the 2021 peak, when pandemic-era enthusiasm pushed registrations to an all-time high.

Most people read this as: Amazon is getting harder to enter. Competition is easing. The barriers are working.

That’s not wrong, but it’s incomplete.

The more important signal is who those 165,000 new sellers are. Chinese sellers represented 59.9% of new launches in 2025, and they crossed 50% of the global active seller base for the first time. US-based sellers accounted for just 16.3% of new launches.

The sellers entering the marketplace in 2025 are not first-time entrepreneurs testing a side hustle with $500 in inventory. They are, disproportionately, export-focused operations with factory relationships, low landed costs, and a cost-of-goods advantage that’s structural rather than circumstantial.

Meanwhile, the sellers who are leaving — the 750,000+ who were “active” in 2021 but aren’t in 2025 — are largely the undercapitalized, the ones who couldn’t weather margin compression, and the ones who never built the operational infrastructure to stay alive through platform changes.

Fewer new sellers doesn’t mean less competition. It means the competition you face has better access to capital and lower costs. That’s a more demanding opponent, not an easier one.

The Two-Tier Marketplace

The concentration data is the clearest signal in all of this.

Fewer than 8,000 sellers — that’s 1.6% of the US active base — drive 50% of US third-party GMV. Third-party sellers now account for 61–62% of all units on Amazon, and US 3P GMV hit approximately $300–305 billion in 2025.

That means roughly 492,000 US sellers are dividing the other half.

100,000+ sellers do $1 million or more per year, up from approximately 60,000 in 2021. At the very top, 235 sellers crossed $100 million in annual sales. This is revenue concentrating at the top in a way that wasn’t true five years ago.

The middle is being squeezed. I’ve watched this play out with sellers in the $500k–$2M range. They’re not failing dramatically. They’re just finding that the same effort that produced comfortable margins in 2020 produces thinner margins today, because the sellers above them have better tools, more catalog depth, and lower COGs.

Two tiers are forming. Tier one: the 8,000 who compete on infrastructure — advertising, supply chain, brand, data. Tier two: the rest, who compete on niche, agility, or low overhead.

The question isn’t whether this consolidation is happening. It is. The question is which tier your business is building toward, and whether your operational choices reflect that.

The Brand Registry Signal

Enrollment in Brand Registry is now a floor, not a differentiator. That’s the thing most sellers in this cohort miss.

According to Amazon’s Brand Protection report, over 800,000 brands are now enrolled in Amazon Brand Registry worldwide. The composition matters more than the raw count. Brand Registry is no longer just a tool for stopping knockoffs. In 2025 and into 2026, nearly every significant Amazon policy change — sponsored brand formats, A+ content access, Brand Tailored Promotions, enhanced listing protections — is gated behind enrollment.

The 800k+ enrolled brands are, in aggregate, the most operationally serious cohort on the platform. They’ve made the investment in trademark registration, they’ve completed the enrollment process, and they’re showing up to use the tools that Amazon keeps adding to the Brand Registry dashboard.

But 800k+ enrolled brands have access to the same brand protection tools. What they don’t have is visibility into what’s actually happening to their listings on a day-to-day basis — unauthorized sellers, content changes, suppression events — in real time.

What Consolidation Actually Means for Your Business

The data says one thing. Most people hear something else.

What sellers tend to hear: “Amazon is consolidating, so it’s harder to break in.” True, but not the point.

What the data actually describes: in a consolidating marketplace, the cost of a listing integrity failure goes up. The margin for error shrinks.

When the rules of Buy Box competition changed in 2025, sellers who weren’t paying close attention woke up to repricing logic that no longer worked the way it used to. When Amazon’s AI systems began making silent listing changes in a more competitive marketplace, brands with no monitoring in place didn’t know until their conversion rate had already moved.

This is the arithmetic of consolidation: if you’re operating in a marketplace where 8,000 sellers are competing on infrastructure, and you’re not in that tier, a single listing event — a hijacker, a suppression, an unauthorized content edit — can cost you a week of revenue and a month of ranking recovery.

In 2021, with lower CPCs and more organic traffic to go around, you could absorb that. In 2026, with advertising costs up and organic share down, you can’t absorb it as easily.

That’s what consolidation actually means for your business. Not just that breaking in is harder. That operational slippage is more expensive, because the competitive environment punishes it faster.

For brands in the Brand Registry cohort — the 800k+ taking the platform seriously — real-time listing intelligence becomes a core operational requirement, not a nice-to-have. SentryKit, our Buy Box intelligence platform, is built for exactly this: flagging what’s changing on your listings before it costs you. That’s the one mention I’ll make here — this isn’t a sales post.

That’s the setup. Here’s what to do about it: decide which tier you’re building toward, and close the operational gaps that tier requires.